Table of Content

If you’re worried about being approved for a better rate, Navy Federal will take alternative factors into consideration, such as a history of making rent payments on time. You may also want to avoid refinancing simply to get a slightly lower interest rate. It takes a significant drop — between 1% and 2% in general — to make the savings worth the extra costs that come with refinancing. You can use a mortgage refinance calculator to help you determine whether refinancing makes sense. Mortgage rates are currently averaging between the high 2% to 3% range, which is far lower than credit cards and even some student loans.

A fixed-rate home equity loan provides you with a lump sum of a cash at a fixed interest rate that won't change over the lifetime of your loan, providing you with predictable monthly payments. With a rate-and-term refinance, borrowers can reduce their interest rate, lower their monthly payments or shorten their term in order to pay off the loan faster. For military service members, Navy Federal’s mortgage refinance rates are extremely affordable and flexible.

Best Mortgage Refinance Lenders

Even if rates are low, however, it’s important to consider your future plans. If you expect to sell your home in the foreseeable future, for instance, it might not make sense to start over with a new loan. A better credit score will help you secure a better rate and make your refinance even more cost-effective.

"Mortgage rates have risen dramatically this year," said Dave Steinmetz, division president of origination services at ServiceLink. "Rising rates can be attributed to Federal Reserve action that has been motivated by a variety of factors, most notably, the need to tamp inflation." The following table lists average HELOC rates in five of the largest US metropolitan cities.

How Do I Qualify for Refinancing?

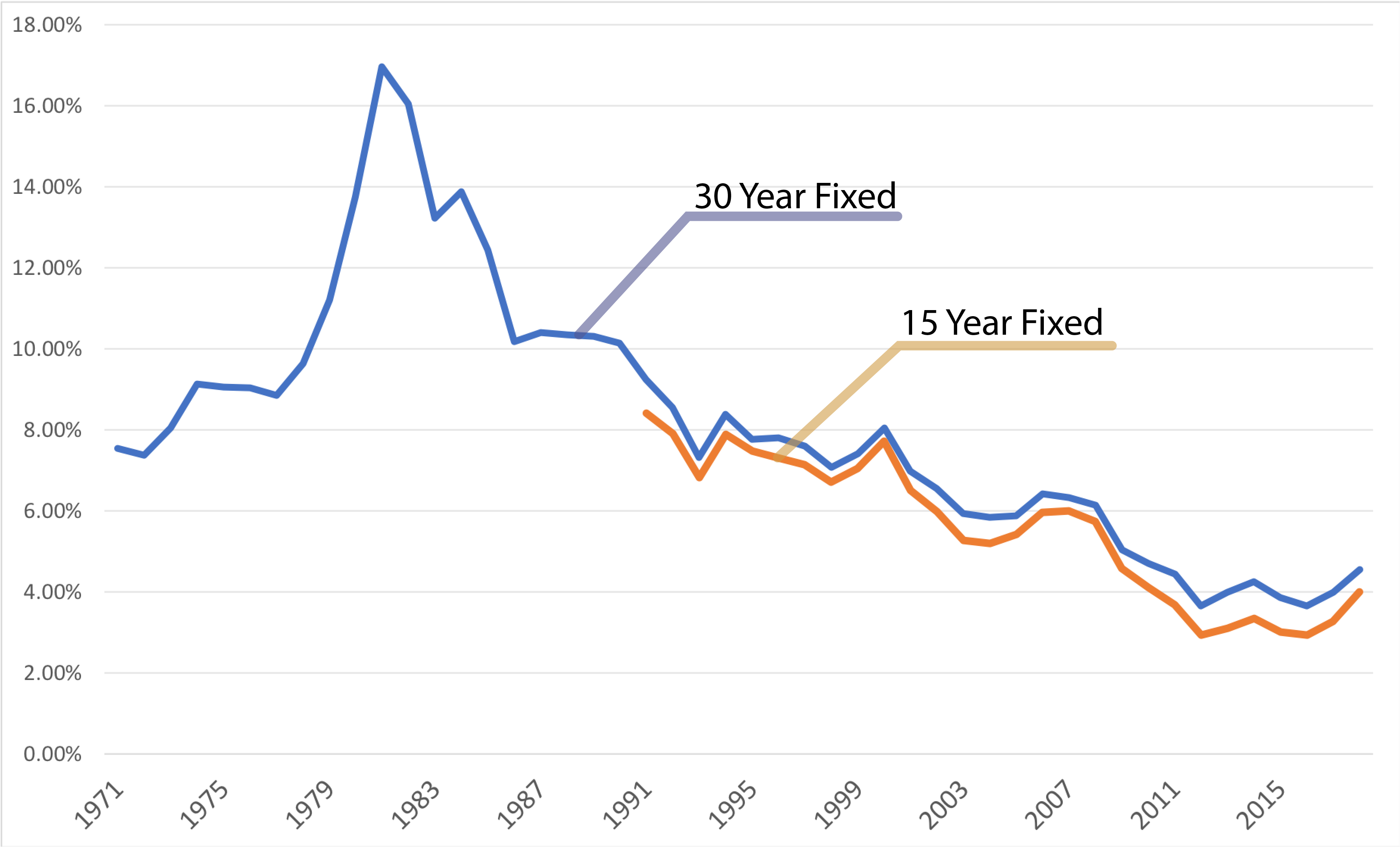

Even though the Fed is likely to increase rates again, now's still a good time to consider taking out a home equity loan. Everything from where the property is located to the type of loan you’re refinancing into can change what you’ll pay to refinance. Take a look at mortgage refinance rates for a number of different loans.

If you're not happy with your credit score or the rates you're being quoted, work on boosting your credit first, then try to refinance again once you've improved it. Typically, mortgage lenders want to see a credit score of 620 or better for a refinance, but there are some refinance options if you have poor credit, including streamline programs. You can improve your credit score by reducing your credit utilization ratio (the proportion of credit you’re using compared to your credit limit) and paying down your highest-interest or highest-payment debt. Now may be a great time to refinance and take advantage of historically low interest rates, even with potential fees or costs involved.

Why should I refinance?

You agree that any such advice and content is provided for information, education, and entertainment purposes only, and does not constitute legal, financial, tax planning, medical, or other advice from Interest.com. You agree that Interest.com is not liable for any advice provided by third parties. To use some of the Services, you may need to provide information such as credit card numbers, bank account numbers, and other sensitive financial information, to third parties. By using the Services, you agree that Interest.com may collect, store, and transfer such information on your behalf, and at your sole request.

She previously reported on retirement and investing for Money.com and was a staff writer at Time magazine. She has written for various publications, such as Fortune, InStyle and Travel + Leisure, and she also worked in social media and digital production at NBC Nightly News with Lester Holt and NY1. She graduated from the Craig Newmark Graduate School of Journalism at CUNY and Villanova University.

A float down option will cost you -- typically 0.5% to 1% of the loan amount -- but it could save you money if rates drop. While lower monthly mortgage payments sound enticing, refinancing isn't always a smart financial move. "The cost of borrowing from home equity has gone up dramatically this year," says Greg McBride, chief financial analyst for CNET's sister site, Bankrate. "Whether you're borrowing through a home equity line of credit, a fixed-rate home equity loan or a cash-out refinance, rates are rising at a very fast pace." Your personal finances aren’t the only factor that impacts the mortgage refinance rate you qualify for. You want to have at least 20% equity, or a loan-to-value ratio of 80% or less.

Generally speaking, for both home equity loans and HELOCs, any rate that's lower than the national average of just below 8% is considered a good rate. Regardless of the type of loan you use, rates are still elevated across the board and will remain high into 2023. "We've seen drastic increases in the rates for all of those avenues for borrowing," says McBride. Loans are fixed-rate loans, so the interest rate will stay steady when the Fed raises or lowers interest rates.

The opinions expressed are the author’s alone and have not been provided, approved, or otherwise endorsed by our partners. The current average rate on a 30-year VA refinance loan is 6.17% compared to 6.10% the week prior. The mortgage must be “net tangible benefit” to the borrower, which is based on the loan rate and term.

Bankrate is compensated in exchange for featured placement of sponsored products and services, or your clicking on links posted on this website. This compensation may impact how, where and in what order products appear. Our advertisers are leaders in the marketplace, and they compensate us in exchange for placement of their products or services when you click on certain links posted on our site. This allows us to bring you, at no charge, quality content, competitive rates and useful tools.

Mike Fratantoni, chief economist for the Mortgage Bankers Association says rates might have already peaked this year, which could provide an opportunity for a few homeowners to refinance. If you are seeking a loan for more than $548,250, lenders in certain locations may be able to provide terms that are different from those shown in the table above. You should confirm your terms with the lender for your requested loan amount. Greg McBride, CFA, is Senior Vice President, Chief Financial Analyst, for Bankrate.com. He leads a team responsible for researching financial products, providing analysis, and advice on personal finance to a vast consumer audience. Angelica Leicht is a writer and editor who specializes in everything mortgage-related for Interest.com.

Explore refinance offers from at least three mortgage lenders , and keep an eye on rates while you comparison-shop — this can help you decide when to lock in a rate. Check out Bankrate's lender reviews, as well, to help guide your decision. She has won several national and state awards for uncovering employee discrimination at a government agency, and how the 2008 financial crisis impacted Florida banking and immigration. A 5/1 ARM, or adjustable-rate mortgage, has an average interest rate of 5.33%. With a HELOC, you can borrow what you need when you need it by writing a check or using a credit card connected to the account.

HELOCs also may give you tax advantages over home equity loans, but you’ll need to research whether or not you’d qualify for these tax breaks. It’s tough to break even with the extra costs after refinancing if you plan to unload the property in the near future. You’d have to see a significant drop in rate, or stay in your home significantly longer than you planned to, for that to be the case. So if you’re planning to move soon, you might want to reconsider the plan to refinance. And if you already have an FHA mortgage, you may qualify for a streamline refinance that requires less credit documentation.

No comments:

Post a Comment